How Does SBTi FLAG Impact Apparel Brands?

9th December 2022

9th December 2022

The Science-Based Targets initiative (SBTi) has developed guidance for measuring and setting targets on Forest, Land and Agriculture (FLAG) emissions. This requires organisations that have, or are currently setting, a Science-based Target (SBT) and have FLAG-related emissions in their supply chains to set a FLAG SBT. This requirement is in addition to the newly termed regular energy/industry SBT.

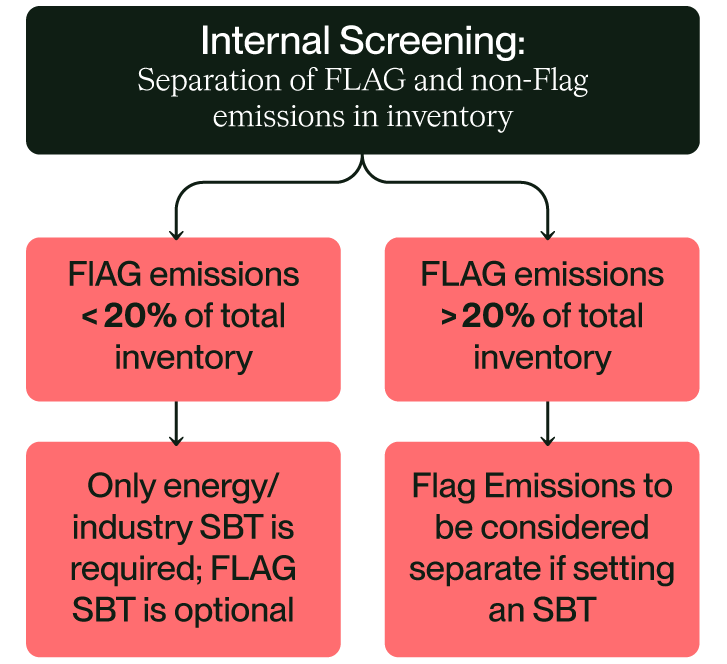

The SBTi FLAG guidance designates several FLAG sectors that are required to report and set targets for FLAG emissions. In addition to these sectors, supply chains where FLAG emissions account for more than 20% of their total gross emissions (across Scope 1, 2 and 3) are required to set a FLAG SBT. Apparel companies are not one of the sectors directly outlined in the FLAG guidance but may fall into the scope if they meet the 20% rule.

There are several exceptions to these rules, for example, if companies in the designated FLAG sectors have limited FLAG emissions (<5%) or are viewed as SMEs by SBTi, they may not be required to set a FLAG SBT.

Apparel brands that have already set or are considering setting an SBT may now also be required to set a FLAG target, so they will need to have visibility on the proportion of their inventory that relates to FLAG emissions.

Companies that are under the scope of the SBTi FLAG guidance will have several requirements:

More specific pathways have been identified for several food sectors, as well as timber and wood and leather. These pathways enable the use of intensity-based emissions reductions and are largely geared towards use by producers. There may likely be some relevance of the timber and wood and leather commodity pathways for the apparel sectors; other emissions, including cotton and other plant-based fibres, will be covered more broadly.

As apparel brands are not directly implicated in the sectors outlined in the SBTi FLAG guidance, there is a requirement for apparel retailers to understand the relative impacts of FLAG emissions on their overall greenhouse gas inventory.

Several materials in a typical apparel company’s Scope 3: Purchased Goods & Services will have FLAG-related emissions, which focuses on the part of the emissions involved in the production of these natural fibres (i.e., agricultural production emissions). The fibres and materials would include, cotton, leather, wool and man-made cellulosic fibres, such as viscose and rayon.

There will be an initial calculation required to screen the emissions of brands to determine whether FLAG emissions meet the threshold of 20% of a brand’s total emissions.

Once this has been determined, companies that have over 20% of their total emissions relating to FLAG activities will be required to set a FLAG target. Different approaches can be taken to set FLAG targets and companies will need to consider which pathway to take depending on the relevant activity and commodities.

Developing targets that focus specifically on forest, land, agriculture and energy emissions enables organisations to focus on the challenges and opportunities associated with those emissions. Forests, oceans, peatlands, and other natural carbon sinks are important in reducing emissions. The FLAG guidance can enable organisations to gain increased visibility of FLAG emissions and an understanding of the types of actions that can be taken to improve practices and use better processes and more regenerative techniques.

Brands under the scope of FLAG will need to follow SBTi’s FLAG guidance to focus on these specific impacts, as well as the typical energy/industry targets that a company has already set for non-land emissions.

The FLAG guidance presents an opportunity to engage with your supply chain further than standard ESG requirements, enabling increased visibility and a more holistic understanding of the carbon impacts down to the farm level. This opens opportunities to drive change on some of the impacts that previously were not visible to many brands, particularly within the apparel sector.

Anthesis offers comprehensive expertise and support to brands that may need to consider setting a FLAG SBT. We can provide clients with a full end-to-end service from initially guiding and upskilling key stakeholders on the FLAG guidance and its implications through to the full screening process required to identify whether a FLAG target is required.

Anthesis supports many organisations to set SBTs and is well-versed when it comes to offering full support towards the SBTi target-setting process. Either before or after setting an SBT, Anthesis can assist in mapping solutions and implementation strategies that help clients reach their intended target, including reviewing potential mitigation strategies around regenerative agriculture and good agricultural practices or more direct targeted supplier engagement programmes which allow brands to track and monitor supplier progress.