Scope 3 Emissions Reporting for AASB S2

Scope 3 emissions reporting for AASB S2 applies from an entity’s second reporting period of mandatory climate‑related disclosures, following a one‑year transition exemption in the initial reporting year. Scope 3 reporting generally involves multi‑source data gathering across the value chain, supplier engagement to obtain primary information, category‑specific estimation methods and careful documentation of assumptions that ultimately need to withstand assurance. Done well, it provides clearer visibility of value chain impacts, stronger supplier relationships, and more informed commercial decision‑making. This article provides practical guidance to help AASB S2 reporters define credible Scope 3 approaches, and prepare disclosures that are transparent, defensible and commercially grounded.

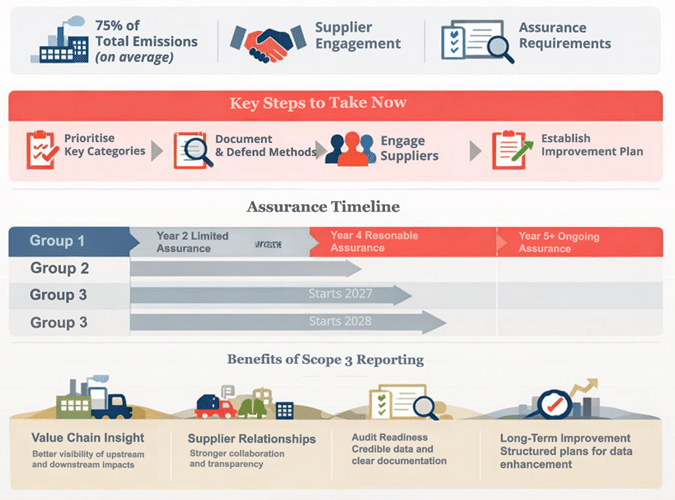

Business leaders recognise that Scope 3 is one of the most complex areas of emissions reporting. It often represents around 75% of a company’s emissions, and calculating impacts across the value chain requires structured approaches, clear methods, and targeted actions, including supplier engagement.

However, visibility also creates value. Measuring Scope 3 emissions improves visibility into where emissions occur across the supply chain, helping organisations identify hotspots, strengthen supplier relationships, and support more informed procurement decisions, resilience, and long‑term performance.

As Scope 3 information becomes more decision‑relevant, it also becomes subject to greater governance and assurance expectations. Scope 3 Emissions Reporting for AASB S2 requires organisations to measure greenhouse gas emissions in line with the GHG Protocol and disclose the methods, boundaries, and estimates that underpin those figures. These disclosures are embedded in annual reporting under the Australian Sustainability Reporting Standards, increasing scrutiny from boards, auditors, and regulators and reinforcing the importance of credible Scope 3 emissions practices.

For an explainer unpacking the basics of Scope 3 emissions read our Comprehensive Guide to Understanding and Reporting Scope 3 Emissions

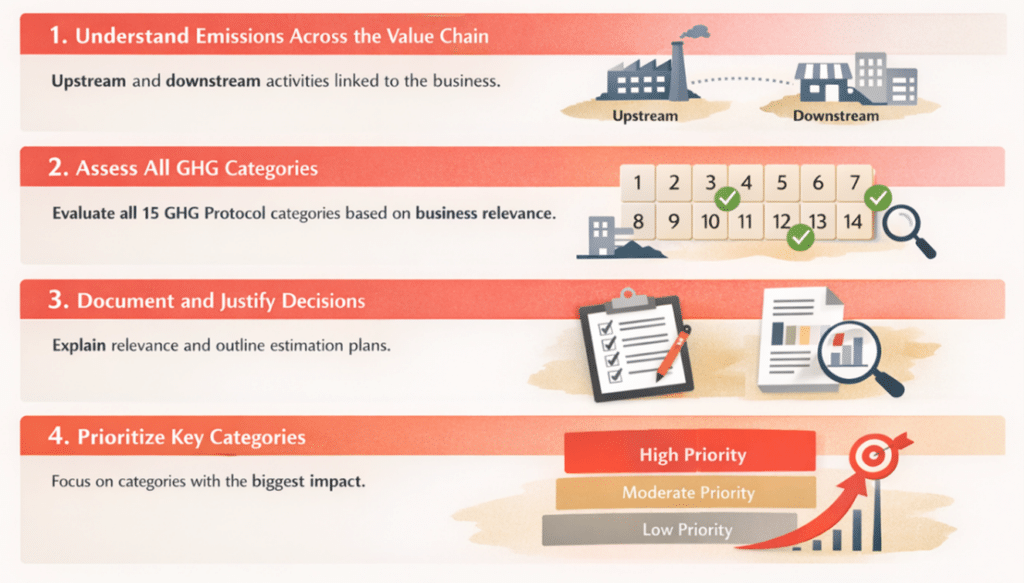

The Scope 3 boundary should reflect where emissions occur across the value chain and how they relate to the business. A clear boundary defines which categories are included and how they are prioritised for estimation, and is anchored in a well‑defined Scope 1 and 2 boundary, which informs Scope 3 relevance. Category coverage should follow the Greenhouse Gas Protocol, as referenced in AASB S2, with transparent reasoning where data is limited, or where estimation will mature over time.

A materiality assessment then applies relevance criteria to determine which Scope 3 categories warrant quantification. This directs effort toward emissions sources that influence exposure, procurement decisions, and reporting relevance, while providing a clear basis for excluding categories assessed as not relevant. Documented rationales for inclusions, exclusions, and prioritisation are critical, as they create a Scope 3 boundary that is transparent, defensible, and able to withstand assurance.

When preparing Scope 3 emissions reporting for AASB S2, companies should document why a category is considered relevant, how it was assessed and how the estimation will be strengthened over time. This creates a transparent process that supports assurance and provides internal clarity. Once the boundary is established, prioritisation can occur within it to focus early effort on the categories that have the greatest operational or strategic significance.

Assessing materiality and relevance directs effort within the defined Scope 3 boundary. It should centre on categories that meaningfully influence emissions, procurement exposure or financial relevance. A practical test considers four lenses:

This provides a decision‑ready way to prioritise categories for early estimation, supplier engagement and improvement planning.

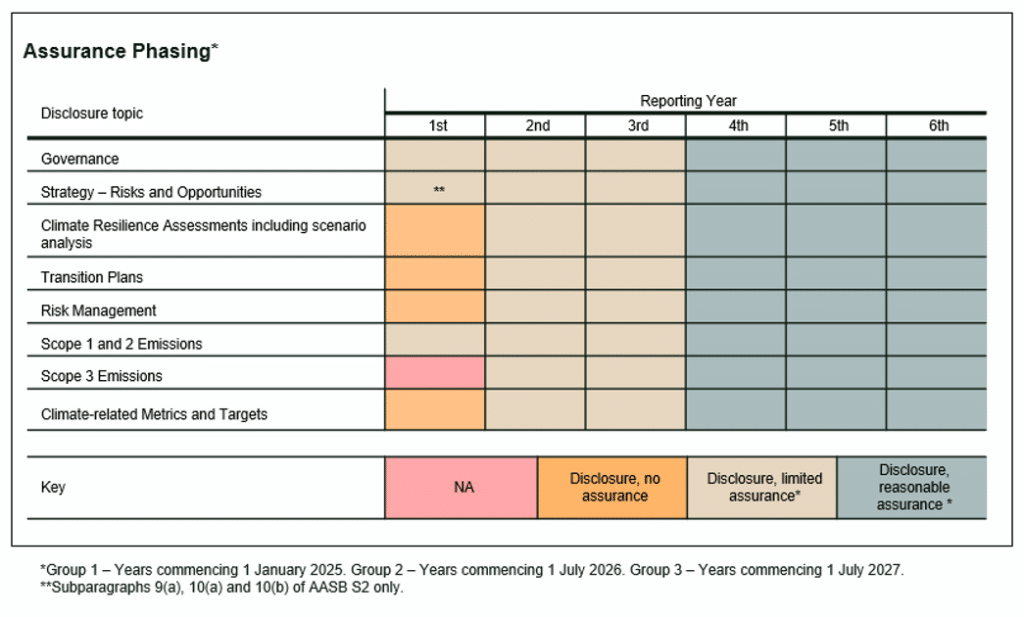

The Auditing and Assurance Standards Board (AASB) has adopted ASSA 5000, with ASSA 5010 setting a staged move from limited to reasonable assurance. Scope 3 disclosure is required from year two of reporting, with limited assurance applying until year 4 when reasonable assurance begins. This translates to the phased assurance timing below. Although this provides some breathing space, starting early strengthens methods, boundaries and evidence, and allows reporters time to get things right, and ensure an adequate boundary and data gathering methods are more robust once assurance is required.

Our experience has shown that estimating a reliable Scope 3 footprint takes years to put appropriate data collection processes in place and to improve data over time through data improvement plans.

Assurance timeline for all groups is:

Group 1 reporters who have to undertake scope 3 emissions reporting for AASB S2, could expect requests for evidence that demonstrates credible boundary setting, transparent methods and a clear plan to strengthen data over time. Auditors may focus on:

The modified liability approach in early years reduces litigation risk for Scope 3, scenario analysis and transition plans, but it does not lower governance expectations. Directors must still demonstrate reasonable steps toward compliance and a clear understanding of how Scope 3 methods and assumptions have been developed.

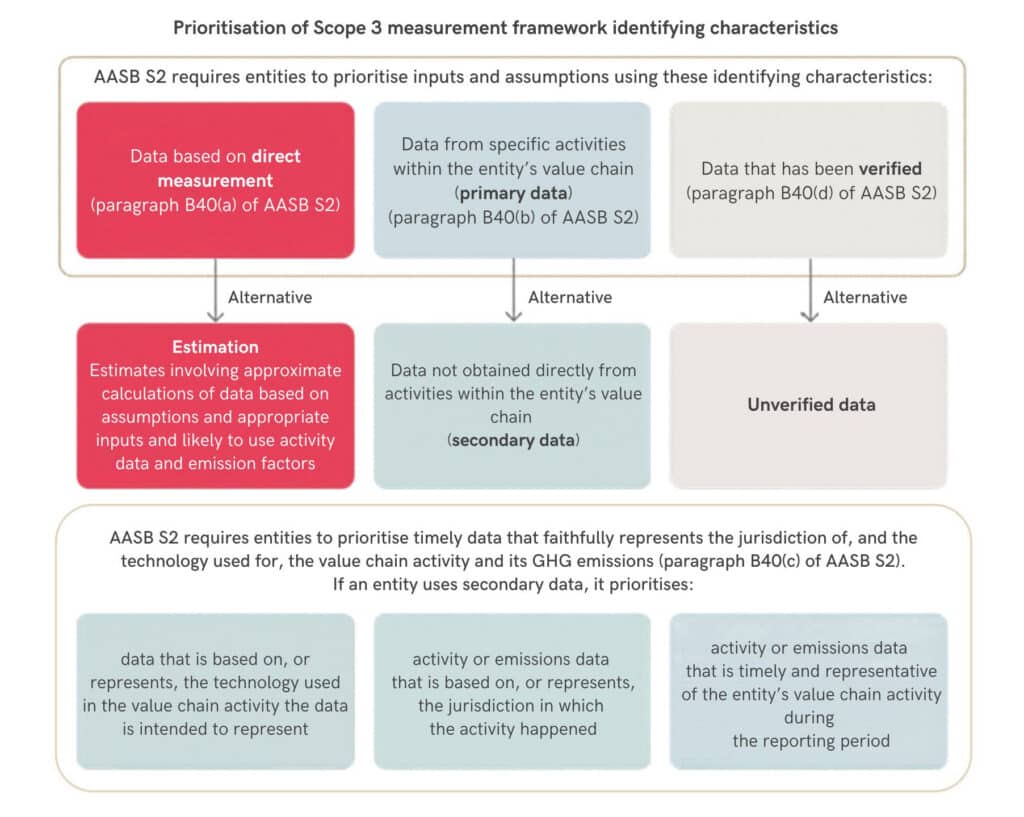

Estimation methods must fit the size and nature of each category. Spend‑based methods, supplier‑specific methods and hybrid approaches all have a place, but reporters need to demonstrate why a chosen method is suitable for the intended use. Assurance standards expect transparent explanations of data sources, emission factors, assumptions and known limitations.

Australian datasets such as National Greenhouse Accounts Factors (NGA Factors) and IELab Footprint Lab emissions factors can support more accurate estimation. NGA Factors provide national greenhouse gas emission factors published by the Australian Government, and IELab offers Australian‑specific environmentally extended input‑output data that maps emissions through supply chains.

Once ready to mature your Scope 3 emissions, and to move away from spend-based calculations to using volume, mass, or more accurate data, investigate the potential to integrate supplier-specific emissions and Product Carbon Footprints into your calculations. This will assist with target-setting and reduce the likelihood and risk of needing to re-baseline for when you do transition to better estimation methods. Getting things right the first time reduces future liabilities.

Digital tools can make Scope 3 reporting more manageable by turning a complex data challenge into a structured, repeatable process. Anthesis Intelligence brings together a set of digital platforms that help organisations capture, organise, and improve Scope 3 data across supply chains and products. These tools combine spend‑based estimates, activity data, and supplier‑specific information to give teams a clearer picture of where emissions sit across the value chain and how they evolve over time.

For example, the supply chain platform allows organisations to start with high‑level estimates across key categories, then progressively deepen data quality by engaging priority suppliers. A sustainability team might begin by identifying that a significant proportion of Scope 3 emissions sit in purchased materials. The platform can then be used to segment suppliers, request primary emissions or activity data from those that matter most, and track improvements year on year.

This supports consistency with the GHG Protocol, creates a clear audit trail for AASB S2 disclosures, and helps move Scope 3 reporting from a one‑off calculation to an embedded capability that informs procurement and risk decisions. While digital tools provide the structure and transparency, specialist advisory input remains important to apply judgement, interpret results, and focus effort where it will have the greatest impact.

Learn more about Anthesis Intelligence

Climate Active reporters preparing for ASRS want clarity on how existing inventories map to AASB S2 expectations. While Climate Active inventories provide a useful starting point, ASRS introduces different expectations that require alignment with AASB S2 and the GHG Protocol.

Confirm that the Scope 3 boundary, category coverage and estimation methods map clearly to AASB S2 concepts, not the Climate Active ruleset. This helps avoid assumptions that may not meet assurance expectations and supports a more defensible Scope 3 position as assurance requirements tighten. Climate Active Technical Guidance remains a valuable reference when explaining organisational boundaries, inclusions and exclusions, including the treatment of embodied emissions.

State clearly when you used spend‑based, supplier‑specific, hybrid or activity‑based methods, and why those choices are reasonable under ASRS. AASB S2 expects transparent explanation of the measurement approach, input sources and assumptions.

To secure alignment for Scope 3 reporting, global hospitality leader EVT focused on translating complex climate data into a clear narrative of commercial resilience. By framing value chain emissions as a strategic priority rather than a compliance burden, they successfully secured buy-in from stakeholders at every level of the organisation. This top-down alignment was met with a robust bottom-up engagement strategy designed to “decode the sustainability word salad.”

Additionally, by stripping away technical jargon and interpreting ESG requirements through the lens of familiar financial and operational terms, EVT empowered their in-house teams to understand the tangible value of their contributions, turning a complex reporting exercise into a shared mission for long-term impact.

Key tip: Start early on the data collection and improvement journey.

Learn more from our webinar on Scope 3 emissions for AASB S2 Webinar Series Mandatory Climate Reporting | ASRS: 3. Scope 3 Emissions.

Be explicit about uncertainty: Acknowledge estimation ranges and known data gaps. Point to your data improvement plan and procurement levers that will close gaps over time, consistent with AASB S2’s decision‑useful framing.

Don’t wait for perfect supplier data: Use credible proxies now. CDP’s work shows most companies struggle with complete Scope 3 data; the discipline is to disclose methods and improve. As they say – don’t let perfect be the enemy of good.

Integrate finance and procurement: Tie categories to spend systems and contract clauses that require supplier disclosures next cycle. This is where capability compounds and assurance gets easier.

Connect to strategy and capital: AASB S2 is not only emissions accounting. It expects disclosure of climate‑related risks and opportunities linked to cash flows, financing and cost of capital. Anchor Scope 3 actions to product, sourcing and investment decisions.

Use digital tools to support consistency: Digital platforms such as Anthesis Intelligence Corporate Footprint help apply estimation methods consistently, track factor sources, document assumptions and strengthen evidence for assurance. These tools also support structured data improvement, enabling organisations to move from proxies to supplier‑specific information over time, and can assist with target-setting by visualising different decarbonisation levers for when the time comes.

A key takeaway from a series of ASRS executive workshops we hosted was that Scope 3 emissions and data came up time and again as a pain point, but also as one of the key opportunities. Several speakers highlighted the need to move away from assumptions, build confidence in Scope 3 reporting, and use live market examples (e.g., commodity price fluctuations) to show the tangible impacts of climate risk.

Greater visibility across the value chain: Scope 3 reporting gives organisations clearer insight into where emissions occur across upstream and downstream activities. This supports better prioritisation of data collection, operational improvements and supplier engagement.

Stronger supplier relationships: Structured Scope 3 processes create a platform for more informed discussions with suppliers. Clear expectations, shared data needs and improved transparency help build long‑term relationships that support resilience and commercial performance.

Better alignment between emissions and business decisions: Scope 3 information helps leaders connect emissions drivers to procurement, capital allocation and product strategy. This enables more informed decisions about cost, risk, and long‑term value creation.

Improved readiness for assurance: Clear documentation of boundaries, assumptions and methods strengthens the evidence base needed for ASRS assurance. Early discipline in these areas reduces rework and builds confidence with auditors, boards and investors.

A foundation for long‑term data improvement: Even where estimates are necessary in early years, Scope 3 reporting encourages organisations to plan structured data improvements year on year. This leads to more reliable information, clearer investment cases and better strategic insight over time.

Scope 3 confidence matters more than Scope 3 perfection. Treat year one as the start of a repeatable, audit‑ready process. Focus on clarity, defensibility and steady improvement rather than exhaustive precision on day one.

These steps build credibility with investors, auditors and regulators and set the foundation for reliable Scope 3 reporting under AASB S2.

Scope 3 disclosures remain one of the more complex components of ASRS, but organisations that embed clarity in their boundaries, methods and evidence will be better prepared for assurance. A consistent focus on transparent assumptions, targeted supplier engagement and year‑on‑year data improvement strengthens the reliability of disclosures and positions organisations to respond to growing expectations from investors, customers and regulators.

Anthesis has supported many of Australia’s largest organisations to prepare for AASB S2, and our team can guide you through the full reporting process or specific elements such as climate‑related risks and opportunities, scenario analysis and Scope 3 reporting. We bring deep technical expertise and more than a decade of experience advising leading global companies, helping organisations build credible, decision‑useful disclosures in this new reporting environment. Call us for a chat on +61 3 7035 1740 to find out more, or reach out to our experts via email or the form below.

Thank you for your interest in Anthesis. Please complete this form to discuss how we can help you.