Regulations Hub

Dive into the world of sustainability regulations, standards and disclosure requirements

As sustainability regulations gain momentum worldwide, navigating compliance and strategic alignment poses a growing challenge for organisations, as they actively incorporate sustainability into their business strategies.

This shift not only emphasises the formalisation of sustainability initiatives but also underscores the importance of enhanced communication and transparency. Understanding the intricate relationships between reporting frameworks, standards, regulations, goals, and investor-focused ratings becomes paramount for companies as they navigate the short, medium, and long-term impacts on their business activities.

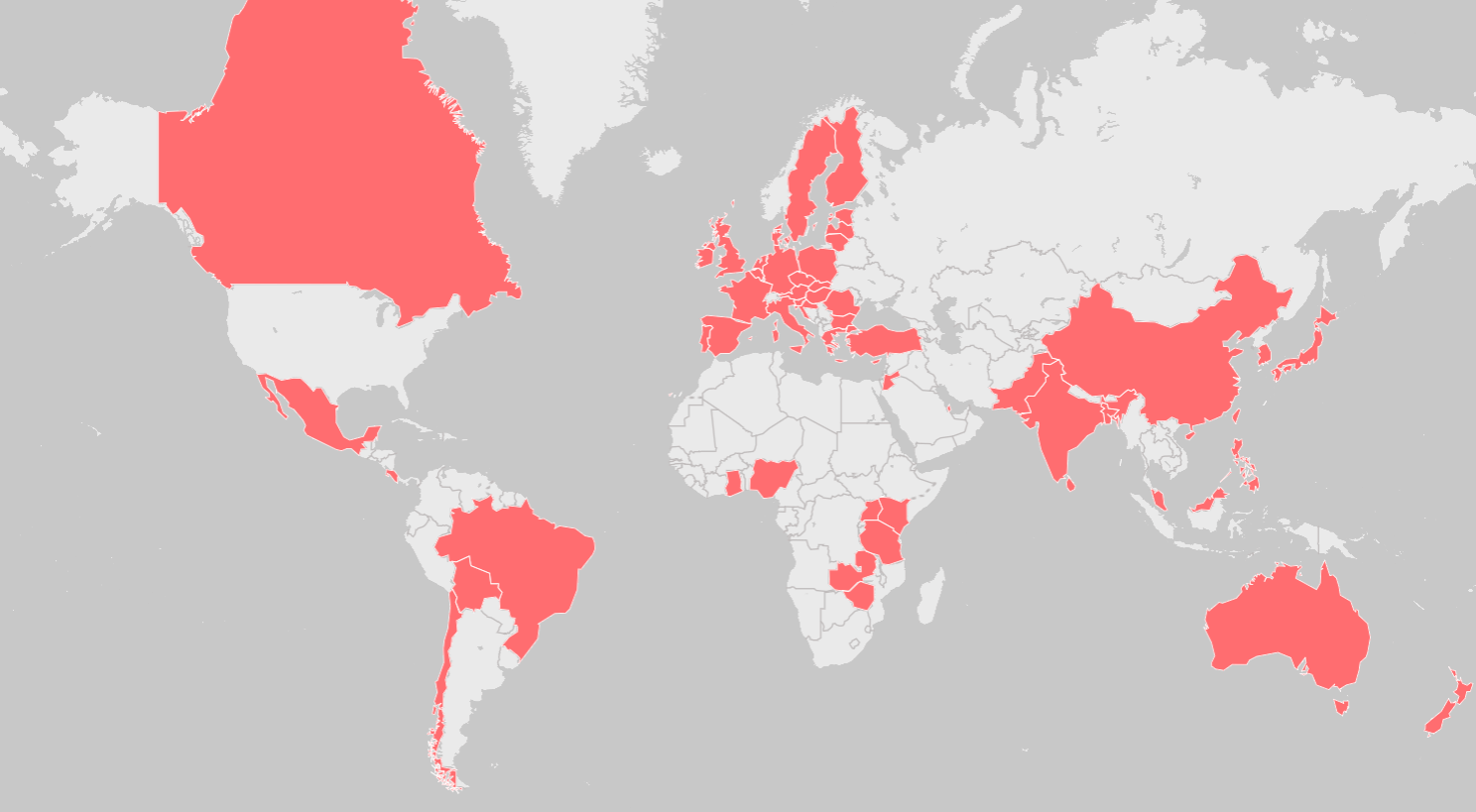

The regulatory landscape is shifting. Use our interactive map to see how the ISSB, CSRD and CSDDD could affect your operations.

We are the world’s leading purpose driven, digitally enabled, science-based activator. And always welcome inquiries and partnerships to drive positive change together.