Sustainability Reporting Singapore: How to Prepare for Mandatory Climate Reporting to the ISSB Standards

An overview on what you need to know about Singapore's sustainability and climate-related disclosures

3 September 2025

An overview on what you need to know about Singapore's sustainability and climate-related disclosures

3 September 2025

Singapore has joined other major global markets in pushing for clearer disclosure of climate risks and opportunities to implement mandatory climate reporting aligned with the International Sustainability Standards Board (ISSB). These disclosures will improve consistency and align corporate practices with global standards, as investors, regulators, and stakeholders demand greater transparency. Climate reporting requirements will be phased in between FY2025 and FY3032 to eventually cover both Singapore Exchange (SGX) listed companies and large non-listed companies.

Whether your organisation falls under Group 1 (reporting from January 1, 2025) or is voluntarily aligning with stakeholder and supply chain expectations, these new standards are likely to affect you. This article answers the most common questions on how to prepare for mandatory climate reporting to the ISSB standards in Singapore, helping you understand the requirements and take your next steps on climate-related financial disclosures.

In 2023, the ISSB, established by the International Financial Reporting Standards (IFRS) Foundation, published a set of standards for sustainability disclosures. These standards were informed by and consolidated several other sustainability disclosure and reporting frameworks, establishing a global baseline for consistent and transparent sustainability reporting aimed to enable investors to make decisions informed by financially material sustainability-related risks and opportunities.

In line with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), the previous best practice framework for climate-related financial disclosures, the ISSB standards are structured through four key disclosure areas:

IFRS S1 – sustainability-related – sets out how companies should disclose governance, strategy, risk management, and metrics related to sustainability risks and opportunities beyond just climate, building on the TCFD framework. In Singapore, IFRS S1 is not mandatory, except for climate-related aspects. For example, companies must disclose climate risks and opportunities that could affect cash flow, financing, or capital costs.

IFRS S2 – climate-related – is mandatory in Singapore and sets out how companies must disclose climate-related risks and opportunities that could affect cash flow, financing, or capital costs in the short, medium, or long term. IFRS S2 subsumes and builds upon the recommendations of the TCFD.

Learn more about the ISSB International Sustainability Standards Board (ISSB) from the IFRS.

All listed companies on the Singapore Exchange must report, with Straits Times Index constituents leading the way, followed by other listed issuers in phases. Large non-listed companies with at least S$1 billion in revenue and S$500 million in assets are also required to report.

The latest update by the Accounting and Corporate Regulatory Authority (ACRA) and Singapore Exchange Regulation (SGX RegCo) in August 2025 introduces an extended timeline for most reporting requirements. This phased approach is aimed at giving companies adequate time to build internal reporting capacity and adapt to ISSB standards.

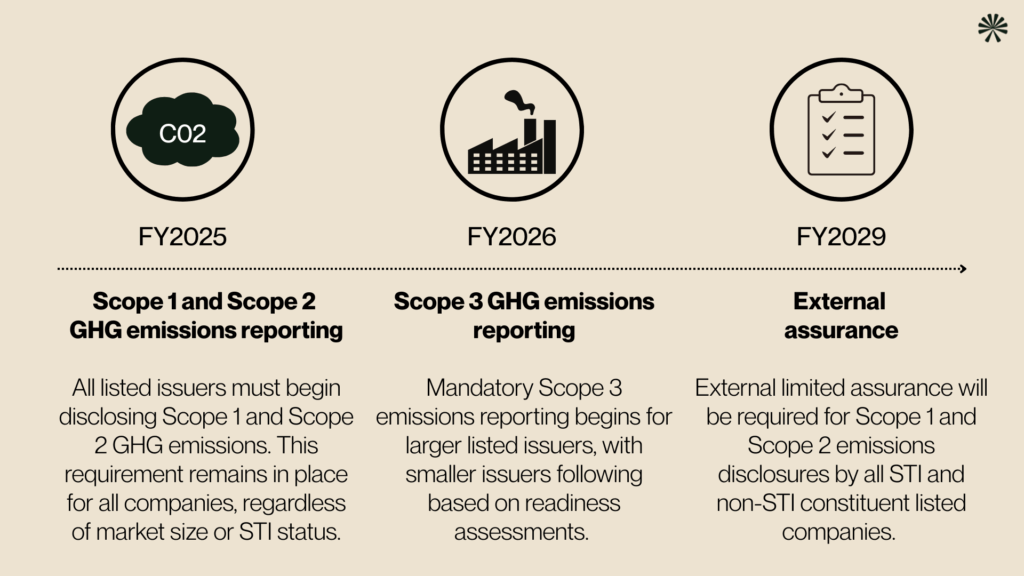

Despite the extended timeline, it is notable that the regulators have maintained the requirements for all listed entities to report Scope 1 and 2 emissions, and for the larger issuers to report Scope 3 emissions for larger issuers by FY2026, This signals a clear focus on driving accountability and transparency on decarbonisation, even as companies are given more time to prepare for other aspects of sustainability reporting.

Due to the latest announcement, the climate reporting timeline is:

This phased approach maintains Singapore’s direction of travel toward consistent and decision-useful ESG disclosures, while acknowledging operational readiness differences across the market.

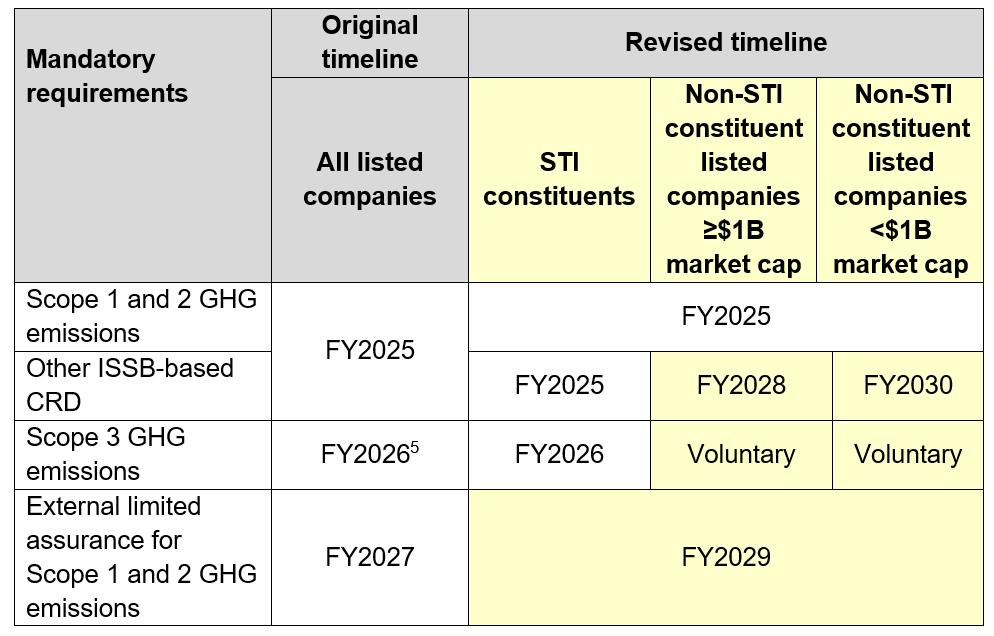

Table 1: Summary of updated climate reporting requirements for listed companies (updates highlighted in yellow). Image: SGX Group

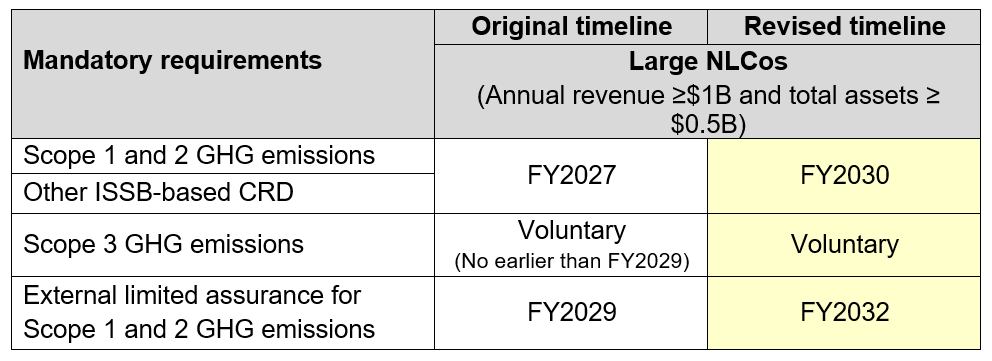

Table 2: Summary of updated climate reporting requirements for large NLCos (updates highlighted in yellow). Image: SGX Group

Yes, there are penalties for non-compliance with mandatory climate-related reporting requirements.

For listed companies, failure to meet disclosure obligations under the SGX rules can lead to regulatory actions by SGX RegCo, such as:

For large non-listed companies, specific penalty frameworks under the upcoming mandatory climate-related disclosure rules are still being clarified, but non-compliance may result in regulatory scrutiny or reputational risk.

Even where not fined, failure to comply can damage investor confidence, affect access to finance and/or new markets, and harm market reputation.

This limited assurance means an independent third party reviews the reported emissions data to provide moderate assurance on its reliability, helping strengthen trust and credibility with investors and stakeholders.

The cornerstone of Singapore’s sustainability agenda is the Singapore Green Plan 2030, launched in 2021. This plan sets ambitious goals such as achieving net-zero emissions by 2050 and is deeply aligned with the United Nations’ 2030 Sustainable Development Agenda and the Paris Agreement. ESG reporting is a practical tool to measure progress toward these national and international goals, ensuring both public and private sectors contribute meaningfully.

Sustainability reporting is also being implemented to increase transparency, align with global standards, and help companies manage climate-related and broader ESG risks and opportunities.

While financial reports reflect past and present performance, sustainability reports provide insight into future risks and opportunities, giving investors and stakeholders a fuller picture of a company’s financial prospects and the quality of its management. Companies that are able to demonstrate they are ahead in their decarbonisation journeys and understand the impact on their business of climate-related risks and opportunities stand to benefit from increased innovation, access to new markets, customers, and financing.

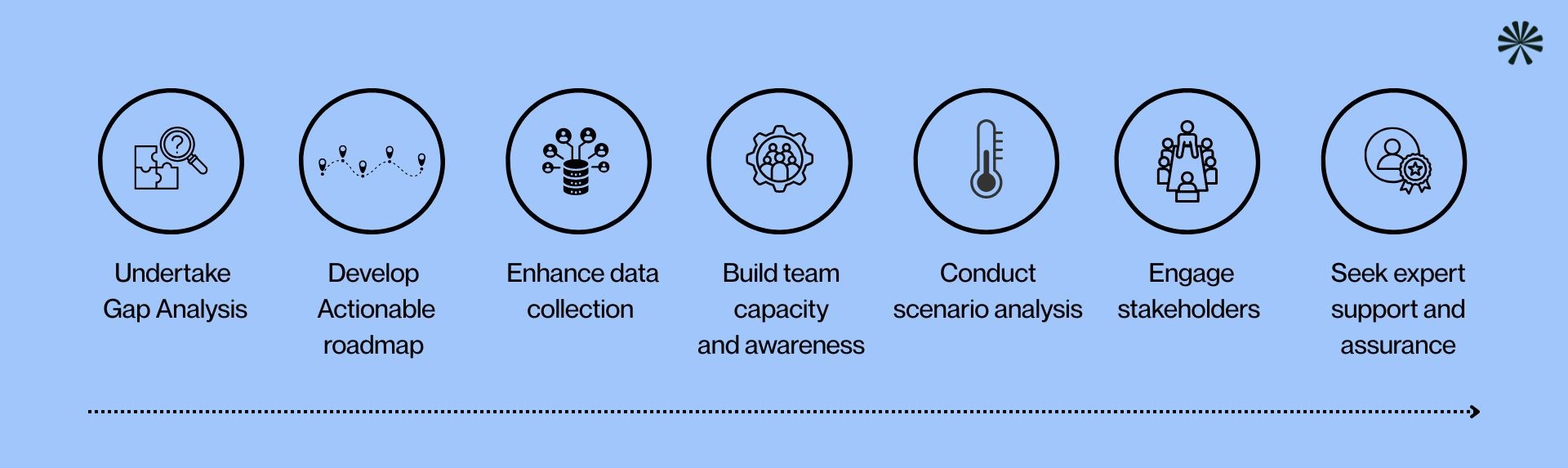

By following these steps, companies can meet regulatory expectations while strengthening resilience, managing climate risks, and enhancing their appeal to investors in a low-carbon economy.

Companies must prepare and publish an annual sustainability report that includes mandatory climate-related disclosures, structured around four pillars:

Listed companies will submit their sustainability report alongside their financial statements, in line with existing reporting timelines. Where external assurance has been conducted, the sustainability report may be issued separately, but no later than five months after the financial year-end.

Note the SGX has an expectation that large issuers will be required to report on Scope 3 GHG emissions and thus the content in their climate reporting will be aligned with the climate-related requirements in the IFRS Sustainability Disclosure Standards for CY26.

The Sustainability Reporting Grant (SRG) is a Singapore government initiative that supports large companies (with revenues above S$100 million) in preparing their first sustainability reports aligned with ISSB standards. It co-funds up to 30% of eligible costs, capped at S$150,000, covering consultancy, assurance, tools, and training. The grant, administered by Enterprise Singapore and the EDB, aims to help businesses meet upcoming mandatory disclosure requirements.

Key benefits of sustainability and climate-related reporting aligned with ISSB standards (IFRS S1 and S2).

As established climate experts globally and in APAC, we offer advice based on years of experience on reporting to regulatory standards and frameworks such as ISSB, ESRS, ASRS, CSRD, and many more, to manage your climate risks, seize opportunities, and drive compliance and sustainable performance across your business now and into the future. We’ll help discover efficiencies, create stakeholder value and increase your positive impact.

Officially licensed by:

")

Anthesis Consulting Group Ltd. licenses and applies the IFRS® Sustainability Disclosure Standards and the SASB® Standards in our work.

Learn more about ISSB standards and how we can support your compliance journey.

We are the world’s leading purpose driven, digitally enabled, science-based activator. And always welcome inquiries and partnerships to drive positive change together.