Early Insights into How Global Companies Are Interpreting ISSB Requirements in Practice

Insights from Anthesis’ Global ISSB Webinar Series

28 May 2026

Insights from Anthesis’ Global ISSB Webinar Series

28 May 2026

More than 40 jurisdictions, representing approximately 60% of global GDP, are moving towards ISSB-aligned reporting. Early insights from organisations already reporting show a clear pattern: the value sits in how disclosures inform decision-making, not compliance alone.

Anthesis convened ISSB representatives, early adopters and practitioners to explore practical lessons from first-year reporting, including AASB S2 disclosures in Australia and broader global insights. A consistent message emerged: organisations seeing the greatest value are using ISSB reporting to strengthen governance, improve decision-making, manage risk and build long-term resilience.

The ISSB standards respond to investor demand for consistent, comparable and verifiable sustainability-related financial information. The purpose of IFRS S1 and S2 is not simply to increase reporting obligations. They are designed to help organisations communicate how sustainability-related risks and opportunities may impact cash flows, access to finance and cost of capital.

The ISSB is progressing work on nature-related disclosures, building on TNFD and the LEAP approach. Rather than introducing an immediate standard, the ISSB recently voted to develop a practice statement to provide greater flexibility for jurisdictions and companies still embedding IFRS S1 and S2. The intention is to build incrementally on existing requirements in IFRS S1 and IFRS S2 without overburdening organisations already navigating first-year implementation challenges.

The ISSB also confirmed that research into human capital-related disclosures has progressed into its next phase, with further decisions expected in the coming months. The ISSB reiterated that companies do not need to wait for topic-specific standards. IFRS S1 already requires disclosure of material information about all sustainability-related risks and opportunities relevant to a company.

Consultations are underway across key industries, including Agricultural products, Electric utilities and Meat, Poultry & Dairy. The ISSB emphasised that SASB Standards are intended to simplify reporting by helping companies focus on the sustainability topics and metrics most relevant to their industry and investors, rather than increasing disclosure burden.

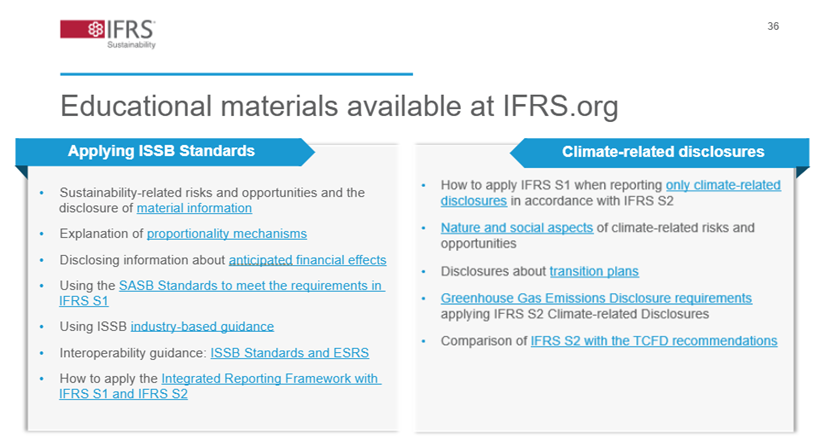

The IFRS Foundation also highlighted the growing suite of implementation resources now available, including:

Anthesis analysed 15 publicly available first-year AASB S2 reports, identifying clear patterns:

Australia’s first wave of reporters have made a serious investment in building the structures required for disclosure, no small achievement given the complexity of first-year implementation. The larger opportunity now is in how those disclosures are used. Risks have been identified, scenarios modelled and governance frameworks established. For organisations preparing to report, building that connection between disclosure and decision-making from the outset will generate significantly more value from the process and better prepare them for the scrutiny that follows.

Orbia grounded the discussion in practical experience, drawing on its first year of disclosure as a purpose-led multinational operating across more than 50 countries and five business groups spanning Building & Infrastructure, Polymer Solutions, Precision Agriculture, Fluor & Energy Materials and Connectivity Solutions.

Orbia’s experience highlighted the importance of building sustainability reporting as a long-term strategic capability, rather than treating it as a standalone compliance exercise. The organisation entered its first year of ISSB reporting in Mexico with strong foundations already in place, including board-level sustainability governance and SBTi-aligned targets across Scope 1, 2 and 3 emissions. However, despite these strong foundations, first-year reporting still presented significant challenges.

In Australia the challenges were similar. For most organisations, the first year of reporting came with a degree of uncertainty. Limited benchmarks and compressed timelines meant teams often took a cautious approach, focusing on what could be supported and defended. But as the process progressed, many clients began to shift how the organisations operate in practice, therefore strengthening governance, improving accountability, and bringing teams together in ways that hadn’t happened before. It also had the benefit of creating much clearer ownership of data and stronger internal understanding of climate across the business.

As organisations embed ISSB reporting into core business processes, a consistent set of challenges is emerging across markets. These reflect the practical realities of aligning sustainability data, governance and reporting with financial and investor expectations.

ISSB adoption is supporting the development of a global baseline for sustainability reporting. This allows organisations to gather data once and apply it across jurisdictions, improving consistency in disclosures and reducing duplication in reporting processes. For multinational organisations, this also provides a clearer foundation for aligning regional requirements and managing increasing reporting complexity.

It is important to remember – first-year reporting marks the starting point rather than the end state. Organisations are building capability over time, strengthening governance, improving data quality and refining how disclosures connect to financial and strategic decision-making. The focus now is on improving depth, consistency and assurance readiness across future reporting cycles.

Not all companies are in the same place. Here is how Anthesis thinks about the stages of the ISSB journey and what each demands:

| Stage | Where You Are | What to Focus On | How Anthesis Helps |

|---|---|---|---|

| Stage 1 Foundation Building | Pre-ISSB; voluntary ESG reporter; TCFD adopter | Gap analysis; governance alignment; materiality assessment; data inventory | ISSB Readiness Assessment; Materiality Assessments; TCFD-to-ISSB Transition |

| Stage 2 First-Year Compliance | Mandatory or voluntary first reporter; 2025–26 go-live | IFRS S1/S2 disclosure drafting; financial impact quantification; scenario analysis | End-to-end disclosure support; climate scenario modelling; assurance readiness |

| Stage 3 Maturation & Integration | Post-first-report; moving toward full S1; assurance preparation | Expand beyond climate; integrate into risk registers; prepare for limited assurance | Nature & social materiality; integrated reporting strategy; assurance support, Climate Transition Plans, Emission Reduction Plans |

| Stage 4 Strategic Value Creation | Advanced reporters linking ISSB data to strategy and capital allocation | Board-ready dashboards; investor-grade data; transition planning; global passporting | Sustainability strategy integration; investor engagement; multi-jurisdiction efficiency |

Most companies in 2025–26 go-live jurisdictions are in Stages 1 or 2. Companies in markets with later timelines can learn from the first wave of reports now available, but they should start building the foundations now.

Anthesis supports organisations at every stage of the ISSB journey – from initial gap analysis through to financial quantification, scenario analysis, assurance readiness and multi-jurisdiction strategy. With over 1,400 experts across 23 countries, official IFRS Sustainability Disclosure Standards licensing and membership of the IFRS Sustainability Alliance, we bring the technical depth and practical experience to move beyond compliance.

If you’d like to sense-check your approach or don’t know where to start, call us for a chat on +61 3 7035 1740 to find out more, or reach out to our experts via email or the form below.

We are the world’s leading purpose driven, digitally enabled, science-based activator. And always welcome inquiries and partnerships to drive positive change together.