How to Navigate Financial Materiality under AASB S2

Navigating financial materiality is a common challenge for organisations preparing for mandatory reporting under AASB S2. We unpack where to focus and what matters most

Financial materiality under the Australian Sustainability Reporting Standards (ASRS) AASB S2 is one of the most challenging topics and one of the questions our clients ask us most about. Sustainability teams want breadth, finance teams want precision, and everyone is asking: what’s truly material?

The frustrating truth is, there’s no universal answer to solve this puzzle. Materiality is nuanced for every company and depends on your organisation’s context and strategic objectives, and requires a level of professional judgement. But, there are principles and tools that can help you move from confusion to clarity and give you and your teams confidence in the decisions you make.

Download exclusive insights from our ASRS Executive workshops on the key insights of preparing for the first year of reporting

What is financial materiality and how does it differ from impact and double materiality assessments?

Firstly, let’s look at the differences between materiality in a sustainability context.

The climate-related reporting standard ASSB S2 focuses on financial materiality (also referred to as investor-focused materiality). It considers only the primary users of the financial sustainability report and requires specific information on a specific risk or opportunity. Disclosures should cover climate‑related risks and opportunities that could reasonably be expected to affect an entity’s cash flows, access to finance, or cost of capital.

A disclosure is financially material if omitting it, misstating it or obscuring it could reasonably be expected to influence decisions of primary users.

Materiality is entity‑specific and requires both qualitative and quantitative judgement.

This differs from an impact materiality assessmentas defined by the Global Reporting Initiative (GRI), which is often used internally to determine which sustainability topics are important to an organisation overall, based on factors such as stakeholder interest, strategic priorities, and potential future relevance. Impact-focused materiality considers the significance of an impact and the likelihood of it to occur on the economy, environment and people, and broad topics are identified as material (e.g. ‘climate’).

While useful for shaping sustainability strategy, an impact materiality assessment does not, on its own, establish whether an issue is financially material for the purposes of AASB S2.

It also differs from double materiality, used in broader sustainability reporting (and global mandatory reporting frameworks such as CSRD and ESRS), where organisations assess not only the financial effects of sustainability‑related risks and opportunities, but also their impacts on the environment and society, irrespective of whether those impacts are currently financially material.

For example, an organisation may conduct a double materiality assessment to identify a wide range of environmental and social impacts across its value chain. While this can inform sustainability strategy and reporting, it does not automatically translate into decision‑useful information for financial materiality disclosure under AASB S2, which requires a specific focus on risks and opportunities with a reasonable expectation of financial effect.

Watch a quick video on materiality for AASB S2.

Why financial materiality under AASB S2 feels so complex

Although financial materiality under AASB S2 has a clear definition, organisations often encounter complexity when translating it into practical disclosure decisions. Here’s where complexity creeps in:

Different internal groups have conflicting views on what matters.

Expectations from primary users of climate-related disclosures (e.g. investors, lenders, and other creditors) and broader stakeholder groups can vary widely. Finance teams often lean on rigid matrices, while sustainability teams push for broader coverage.

Financial materiality in sustainability reporting not only focuses on quantified metrics but also on the question what material information is. Determining what constitutes material information is a challenge.

Not all entities have primary users as defined in AASB S2 (e.g. investors, lenders and other creditors) as they are either owned by an overseas company or are member-based entities. To determine the materiality of information disclosed in these cases can become an issue, as the information requirements of these stakeholders might differ to that of primary users. The task then becomes one of answering the key question who the sustainability report is for within these stakeholder groups.

On top of this, organisations need to understand and communicate the differences between financial reporting materiality and sustainability reporting materiality as discussed earlier.

Timescales can make risk and finance teams feel uncomfortable

Financial reporting traditionally focuses on short-term financial performance, while sustainability reporting considers longer-term risks and opportunities that may not yet be reflected in financial statements. The future-focussed approach brings with it a level of uncertainty that is not something finance teams are generally comfortable with. Clarifying this distinction internally helps avoid confusion and conflicting expectations.

When assessing financial materiality, start with your north star: primary users

Under AASB S2, your North Star is clear: disclosures must serve primary users of general-purpose financial reports, existing and potential investors, lenders, and other creditors.

The International Sustainability Standards Board of which the Australian standards are based on includes similar phrasing:

ISSB Accompanying Guidance IB6: “The objective of IFRS S2 is to require an entity to disclose information about its climate-related risks and opportunities that is useful to users of general purpose financial reports in making decisions relating to providing resources to the entity… However, the responsibility for making materiality judgements and determinations rests with the reporting entity for all requirements”.

And “ The definition of material information is aligned with that used in IFRS Accounting Standards—that is, information is material if omitting, obscuring or misstating it could be reasonably expected to influence investor decisions.” IFRS FAQs.

Internal debates often arise when other stakeholder groups push for inclusion, but compliance decisions should prioritise these defined users. Example: even if your entity does not believe it is exposed to a particular climate risk, you may still need to disclose if your primary users would expect exposure.

This doesn’t mean ignoring other stakeholders entirely. If customers or communities matter for strategic reasons, consider voluntary sustainability reporting (i.e. GRI aligned) but keep mandatory compliance focused on primary users.

Practical steps:

Identify your primary users (investors, lenders, creditors).

Map their financial and strategic priorities.

Engage investor relations early in the process.

Engage with external advisors and auditors to validate your approach.

Make it a whole-of-business process. Bring stakeholders on the journey from the beginning for more buy-in and better outcomes.

Develop clear governance oversight of sustainability reporting which should include policies, processes and scheduled reviews (e.g. Management, Executives, Internal auditors and legal team) to determine what material information to report on.

Remember: omitting, misstating or obscuring information that could reasonably be expected to influence primary users’ decisions is not compliant with AASB S2 disclosures and must be avoided.

“Financial materiality can feel complex, particularly in the context of evolving sustainability reporting expectations. However, organisations that apply a structured decision making approach and anchor materiality judgements to the primary users are better positioned to produce disclosures that are both decision useful and defensible.”

Gregor Theinschnack, Principal Consultant, Anthesis

Inshort, AASB S2 requires entities to disclose decision-useful, material information about climate-related risks and opportunities that genuinely affect financial prospects. Entities must think across the full value chain, focus on primary users’ needs, and ensure disclosures are clear, connected and free from noise.

AASB Guide to the disclosure of material information

When navigating financial materiality – move beyond the matrix

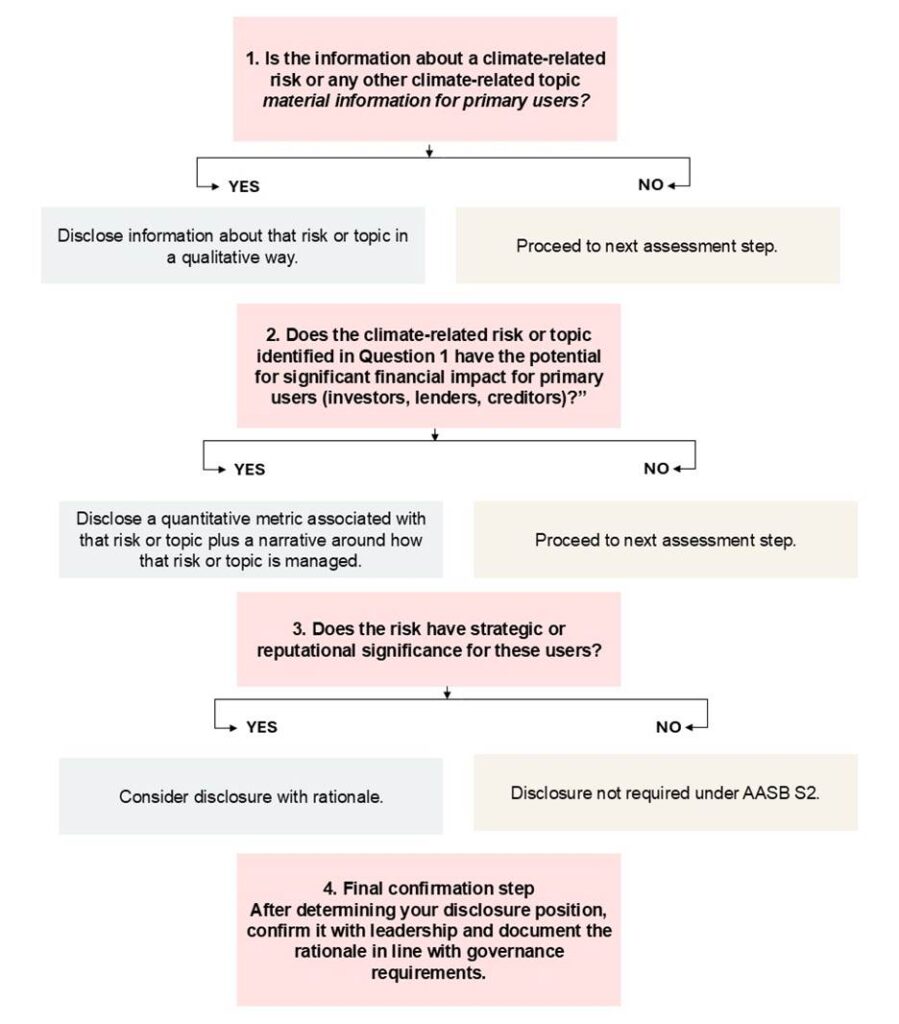

A risk matrix is essential – but won’t solve nuanced debates. Instead, consider building a decision tree that factors in financial impact and strategic significance for primary users. This will help your teams navigate complexity and make consistent calls.

It is also important to apply this decision tree to all elements of the climate-related disclosure which might include disclosure on GHG emissions or any other information that might be material for primary users to understand the overall approach an entity is taking in managing its climate-related risks and opportunities.

Below is a simple sample logic. Before answering Question 1, assess whether the climate‑related risk or topic could reasonably influence the decisions of investors, lenders or creditors. Use your existing enterprise risk assessments, materiality assessments or board‑level priorities as a reference point.

The decision tree offers a simple and practical way to work through financial materiality under AASB S2, guiding your organisation from initial identification of climate‑related risks through to disclosure decisions, while supporting alignment across finance, sustainability and governance teams.

There are also materials and guidance from the regulators that will help support these discussions such as:

Financial materiality – key considerations for disclosure under AASB S2

When preparing disclosures under AASB S2, organisations need to balance transparency with relevance making sure what they report is proportionate, well-governed, and aligned with stakeholder expectations.

Internal Analysis vs External Disclosure

Proportionality Mechanism

Qualitative vs Quantitative Assessment

Investor Relations

Internal Audit

Documentation of Processes

Board Oversight

Governance of Reporting

Embedding these considerations early helps avoid last-minute surprises and ensures disclosures meet both regulatory and stakeholder expectations.

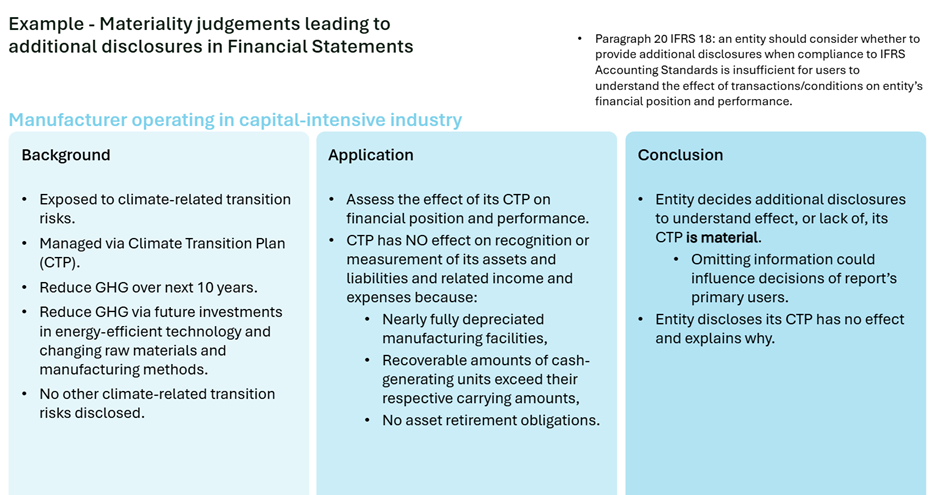

We’ve seen this challenge play out across sectors. The following examples are proposed illustrative examples from the International Financial Reporting Standards (IFRS) exposure draft on Climate-related and Other Uncertainties in the Financial Statements. These represent some of the challenges and key considerations entities can make when applying financial materiality to sustainability reporting.

The first one looks at that at how the mitigating actions, in this case a Climate Transition Plan, can affect a company’s prospects and how that company makes decisions on whether to include more detailed information around that Plan or not.

Below, the example is similar but for a different entity with lower GHG emissions with even less impact on the company’s finances. In the end, the company decides not to include any disclosures in its report on the effect of lack of its GHG policy.

Noting that the materiality decision here to not disclose the effect of its GHG policy does not remove the requirement to disclose its GHG emissions in the Metrics & Targets pillar, and actions the company is taking to mitigate its GHG emissions in the Strategy pillar.

Key takeaways on financial materiality under AASB S2

Materiality under AASB S2 involves a strategic conversation that looks different for every organisation.

Done well, it becomes a tool for aligning sustainability with value creation.

Key things to remember:

Be clear on the difference between materiality in financial reporting and sustainability reporting. They serve different purposes, and the assessment approach differs, even when they use similar concepts.

Financial materiality under AASB S2 uses the same definition as financial reporting, but the way it is applied in a sustainability context is different. Sustainability disclosures often require a wider lens, more forward‑looking judgement and closer engagement with risk, strategy and governance.

Engage with investors, external advisors and auditors early to get a better understanding of how to navigate materiality for your business.

This is a whole-of-business process. Bringing stakeholders on the journey from the beginning = more buy-in and better outcomes.

Develop internal processes to assess, evaluate and analyse climate-related risks and opportunities.

Prepare a “dry run” and involve all relevant stakeholders.

How Anthesis can help navigating materiality for AASB S2

If you’re grappling with this the concept of financial materiality or reporting to AASB S2, Anthesis can help you move from confusion to clarity by building frameworks and facilitating sessions that work for your stakeholders and your business.

Start building resilience today and reach out for advice. We guide businesses through the ASRS landscape to understand their climate risks and opportunities and offer practical, actionable strategies that turn risk management into a strategic advantage and long-term value creation. Call us for a chat on +61 3 7035 1740 or reach out to our experts via email or this form below.

What our clients say

“Working with Anthesis on this project has been a pleasure. Despite the complexity and numerous moving parts of the process, the team kept us on track and ensured our materiality assessment ran incredibly smoothly. The feedback from within our business has been overwhelmingly positive. Your subject matter expertise, guidance, professionalism, and responsiveness were invaluable. Thank you for making this a truly collaborative and rewarding process.”

Materiality Assessment with Great Southern Bank

Explore ASRS Support

We’re trusted guides to some of Australia’s largest companies in preparing for mandatory climate-related disclosures.

We are the world’s leading purpose driven, digitally enabled, science-based activator. And always welcome inquiries and partnerships to drive positive change together.