Understanding Sustainability Reporting in the Philippines – PFRS S1 and S2

The Philippines has officially joined the global movement toward standardized ESG transparency by mandating sustainability and climate-related risk/opportunity disclosures. These new requirements, which align with the International Sustainability Standards Board (ISSB) IFRS S1 and S2, are designed to enhance corporate transparency and bring Philippine businesses in line with international investor expectations. Under the oversight of the Securities and Exchange Commission (SEC), a phased implementation will begin in FY2026, initially targeting the country’s largest publicly listed companies before expanding to other listed and large private entities through 2029.

The shift toward Philippine Financial Reporting Standards (PFRS) S1 and S2 standards is driven by three primary objectives:

For companies who have to report, this a strategic opportunity to think about preparation beyond compliance – to increase market credibility, identify new opportunities, refine risk management practices, and uncover new avenues for capital, such as green financing and climate-focused bonds.

Whether your organization is part of the Tier 1 mandatory rollout for 2027 or is facing pressure from supply chain partners and lenders to report voluntarily, proactive preparation is essential. Understanding the specific requirements of PRFS S1 and S2, and establishing data collection processes now, will ensure your business remains competitive and resilient as regulatory scrutiny intensifies.

The Philippine Financial Reporting Standards (PFRS) will serve as the nationwide framework for sustainability and climate reporting, ensuring that corporate disclosures remain transparent, consistent, and globally comparable.

By issuing Memorandum Circular No. 16, Series of 2025, the SEC has officially integrated the International Sustainability Standards Board (ISSB) framework into local requirements. This adoption introduces two primary pillars:

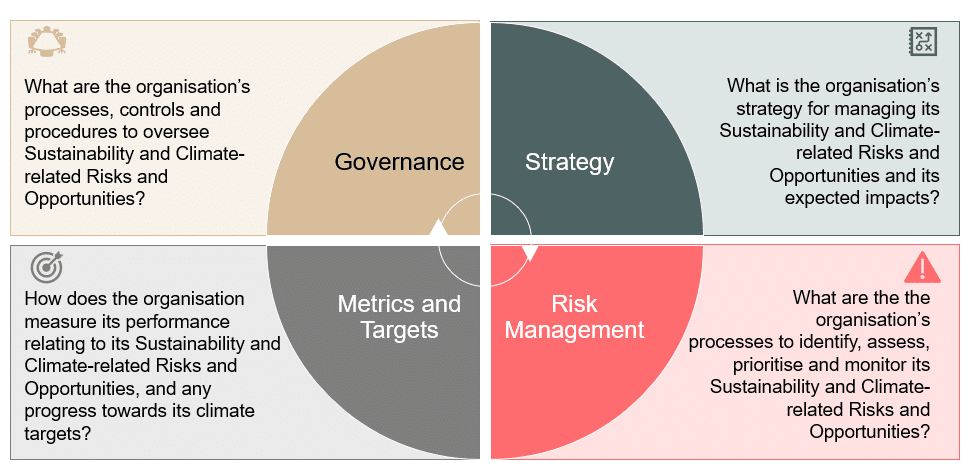

These standards draw directly from the IFRS Foundation’s sustainability reporting standards with the intention to equip investors with information on financially significant sustainability-related risks and prospects. The PFRS (and ISSB) frameworks are divided into four disclosure pillars summarised below (and explained in greater detail later in this article).

The transition toward mandatory sustainability reporting in the Philippines is a strategic move that integrates seamlessly with broader national objectives, such as the Philippine Development Plan 2023–2028. By embedding climate resilience and sustainability into the country’s core economic priorities, this reporting framework serves as a key mechanism for achieving the targets set out in the Paris Agreement. Specifically, it supports the Philippines’ Nationally Determined Contribution, which pledges a substantial reduction in greenhouse gas emissions by 2030, contingent upon international cooperation and support.

Furthermore, these disclosure requirements are deeply rooted in the National Climate Change Action Plan and the emerging National Adaptation Plan. These policies prioritize climate risk management, adaptation strategies, and the expansion of sustainable finance. By aligning with these frameworks, sustainability reporting goes beyond a compliance task to act as a transparent tool to monitor progress toward national climate goals, mobilize the private sector toward net-zero targets, and enhance the country’s appeal to global sustainable investors.

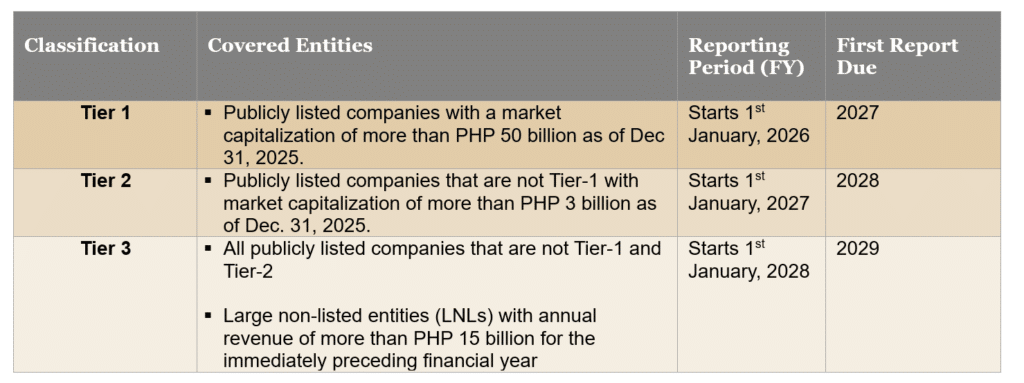

Under SEC Memorandum Circular No. 16, Series of 2025, the Philippine Securities and Exchange Commission (SEC) has transitioned from a voluntary “comply or explain” model to a mandatory sustainability reporting framework. This requirement applies to Publicly Listed Companies (PLCs) and Large Non-Listed Entities (LNLs), with the rollout structured in three tiers based on an organization’s size and market impact.

A distinct set of guidelines and schedules for sustainability reporting will be mandated for government-owned and controlled corporations (GOCCs) classified as Commercial Public Sector Entities, as well as organizations under the jurisdiction of the Insurance Commission. While these entities are currently exempt from the standard tiered rollout, the SEC and relevant regulators will soon issue specific frameworks tailored to their unique operational structures.

All reports must be reviewed and approved by the organization’s Board of Directors prior to submission.

For PLCs and certain regulated organizations, this report is filed as an attachment to the Annual Report, while other large non-listed entities must submit it alongside their Audited Financial Statements.

To ensure a manageable transition, the SEC has established a phased implementation schedule, with compliance deadlines determined by each organization’s specific tier classification.

Despite these separate timelines, organizations are encouraged to initiate the alignment of their disclosures with PFRS S1 and S2 early.

By adopting these standards ahead of the formal deadlines, entities can proactively develop their internal technical capabilities and establish themselves as leaders in sustainability and climate transparency. This early adoption phase provides a strategic window for companies to refine their data collection processes and governance structures, ensuring a smoother transition to mandatory compliance while signalling a strong commitment to sustainable practices to the global market.

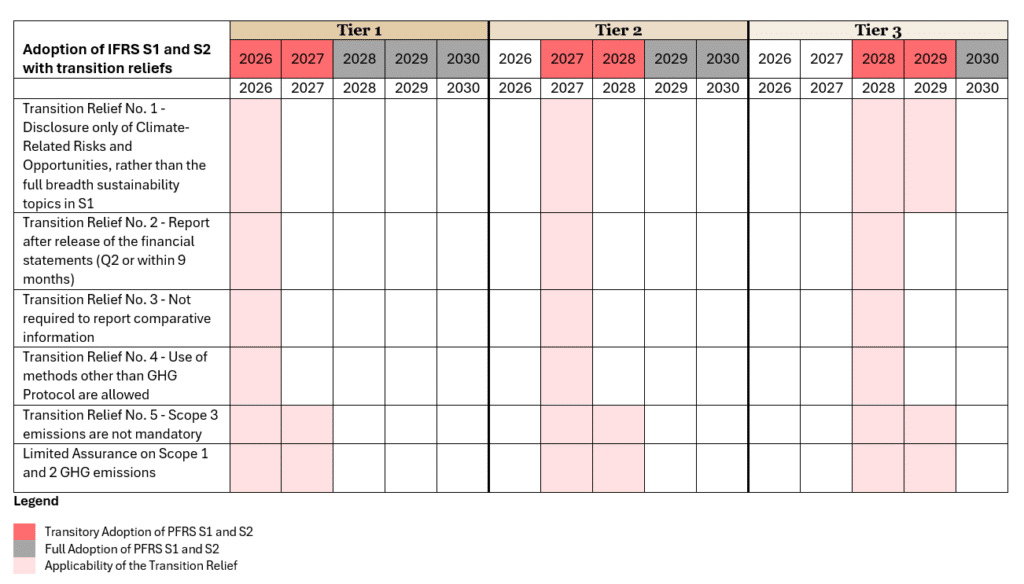

Critically, the SEC’s adoption of PFRS S1 and S2 comes with “transition reliefs” that materially reduce what an in-scope company must do in its first two years of applying the standards.

These reliefs enable a climate-first report for the first year (applicable to Tiers 1 and 2), meaning entities can choose to disclose only their material climate-related risks and opportunities under PFRS S2, rather than the full breadth of sustainability topics under PFRS S1.

For the first year, all entities can omit comparative information, defer publication timing by a few months, and use a GHG measurement methodology different from the GHG Protocol. For the first two years, entities can omit their scope 3 omissions from reporting.

These reliefs are intended to reduce the immediate technical burden on companies while steering the market toward high-quality disclosures.

The specifics of this phased rollout and the related transitional exemptions are detailed below:

The SEC emphasizes that sustainability reporting is a critical tool for ensuring corporate accountability, particularly regarding the national commitment to achieving net-zero emissions. Consequently, the SEC has established a clear enforcement framework: any failure to provide these disclosures will be treated as an Incomplete Annual Report.

Under the guidelines of the SEC Memorandum Circular No. 6, Series of 2005 (the Consolidated Scale of Fines) and SEC Resolution No. 581, Series of 2021, non-submission or late filing of sustainability reports will trigger specific financial penalties. Notably, these violations are subject to a separate scaling of penalties distinct from standard filing fees to reflect the significance of sustainability and climate data. For large non-listed companies, the exact penalty structures will be defined in subsequent official issuances by the Commission.

PFRS requires that entities submit a sustainability report alongside their annual financial report. The requirements of this disclosure is organized into four primary pillars, consistent with global standards. Below is a detailed summary of the regulatory expectations for each:

Disclosures are subject to materiality considerations in a way consistent with ISSB’s Standards around “material information.” That is, reporting organizations are required to disclose material information about the sustainability- and climate-related risks and opportunities that could reasonably be expected to affect the entity’s prospects. Information is considered material if omitting, misstating or obscuring that information could reasonably be expected to influence decisions that primary users of general-purpose financial reports make on the basis of those reports. ‘Materiality’ is therefore an entity-specific measure of relevance, and so entities will need to determine and apply their own materiality thresholds in their assessments.

See how companies are navigating the concept of materiality for disclosures, under the IFRS aligned Australian AASB S2 standard How To Navigate Financial Materiality Under AASB S2 | Australia

In the Philippines, sustainability reports developed in accordance with PFRS S1 and S2 must be submitted to the SEC as a formal component of a company’s annual disclosure obligations. These reports are typically filed as an integral part or an annex of the Annual Report, utilizing the specific electronic filing systems and formats mandated by the Commission.

To ensure high-level accountability, the report requires formal approval from the Board of Directors and must be strictly aligned with the company’s financial statements. While companies must generally adhere to standard statutory filing deadlines, the SEC has provided transitional arrangements during the initial implementation years to help entities adjust to the new reporting cycle.

In the Philippines, sustainability reports under PFRS S1 and S2 are submitted in line with the organization’s annual SEC filing deadlines.

Reporting is phased in by tier:

To ensure these disclosures carry the same weight as financial data, the sustainability report must be submitted in conjunction with the company’s Annual Report. Furthermore, the document requires formal endorsement and approval from the Board of Directors, cementing sustainability oversight as a core governance responsibility.

Note that one of the transition reliefs available to first-year reporters offers several months of timing deferment for submission (see transition relief #2 above).

External assurance requirements will be introduced through a phased approach to allow companies to build the necessary internal data controls. Specifically, an independent practitioner must provide limited assurance on Scope 1 and Scope 2 greenhouse gas emissions two years after an organization’s respective tier begins its mandatory reporting cycle.

While the initial mandate focuses on limited assurance for emissions, the SEC may intend to transition toward a reasonable assurance standard over time.

It is useful however, for companies to consider being proactive and getting voluntary limited or reasonable assurance over their full sustainability report. This provides a clearer signal of accountability and gives stakeholders greater confidence in the quality of the information being reported. Ensuring disclosed sustainability and climate data is verified to assurance standards can also safeguard reporting entities against greenwashing risks, refine internal data-driven decision-making, and potentially some competitive advantages.

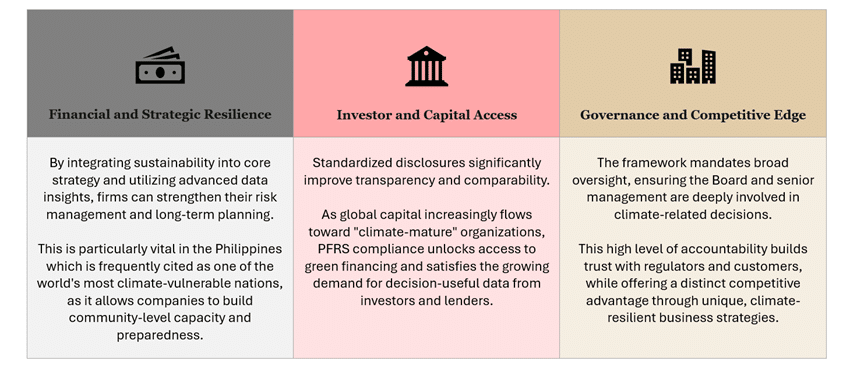

Adopting the PFRS S1 and S2 standards helps organisations build a clearer view of their climate‑related risks, strategic exposures and operational implications under S2, together with a consistent reporting foundation under S1. The alignment with the global ISSB framework provides a common structure that connects local reporting with international investor expectations. Using this framework gives companies a more reliable way to identify gaps in current practices and to prioritise the areas that need attention.

Key strategic benefits of this alignment include:

As globally recognized sustainability and climate experts with strong regional expertise in APAC, we leverage years of experience in regulatory frameworks like ISSB, ESRS, and CSRD to help organizations manage climate risks and capitalize on emerging opportunities. Our mission is to transform compliance into a driver for sustainable performance, operational efficiency, and long-term stakeholder value.

Navigating these complex requirements for the first time can be daunting; however, our team provides the technical depth and implementation experience necessary to move beyond simple compliance. Reach out in the form below.

When partnering with clients, Anthesis delivers a comprehensive suite of strategic services:

Gap Analysis & Strategic Roadmaps: Designing actionable paths to full compliance.

Risk & Opportunity Assessments: Providing qualitative and quantitative insights into climate and sustainability factors relevant for your organisation.

Financial Impact Analysis: Quantifying risks and opportunities to determine their effect on your business model and financial performance and to determine financial materiality thresholds.

Reporting Excellence: Ensuring your disclosures meet both local SEC mandates and global best practice. The adoption of PFRS S1 and S2 in the Philippines represents a significant milestone and is a crucial start for organizations.

Our support goes beyond helping clients with their initial filing. We work with organisations to develop inaugural sustainability reports that meet IFRS/PFRS requirements and present information clearly and consistently. By combining reporting expertise with practical communications support, we help teams translate sustainability and climate data into accessible insights that align with their brand and are easy for stakeholders to understand.

Officially licensed by:

")

Anthesis Consulting Group Ltd. licenses and applies the IFRS® Sustainability Disclosure Standards and the SASB® Standards in our work.

Learn more about ISSB standards and how we can support your compliance journey.

We are the world’s leading purpose driven, digitally enabled, science-based activator. And always welcome inquiries and partnerships to drive positive change together.